Summary: SpaceKnow’s Chinese Automotive dataset provides an in-depth look at the leading automotive market of the world.

China experienced a tough year in 2022. The country had several widespread lockdowns, affecting the economy. Finally, China gave up the zero-Covid strategy late last year. The economy continues to face long-term issues, such as the property downturn and inflation, leading the central bank to cut interest rates.

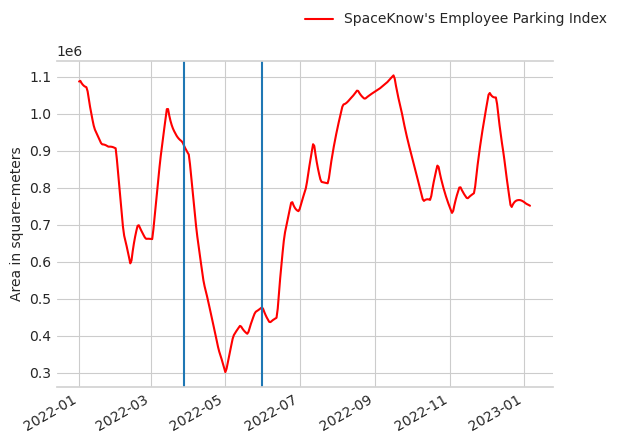

The impact of China’s COVID strategy did not spare the car industry, hitting some of the best-known players, such as US-based carmaker Tesla, which has been rising strongly in recent years. Figure 1 shows Tesla’s Shanghai factory struggling with the Zero-Covid policy in 2022, using Spaceknow’s Continuous Feed Index to monitor the company’s employee parking lots. The factory was affected by the first lockdown shortly after its opening in 2020, but the struggle continued in 2022. The first of the blue vertical lines in Figure 1 is on March 28, the 2022 Shanghai COVID-19 lockdown date. After this date, we see a significant drop in the Spaceknow index – with the lowest point around the day of its reopening (April 19) when Tesla only had a single shift for production. The index rose after May 31, 2022, when normal production resumed.

China’s automotive industry itself seems to be at a crossroad. After years of spectacular growth, creating the world’s largest automotive market by both demand and supply, the slowing Chinese economy is expected to affect demand. This situation is exacerbated by the car industry’s own troubles such as persistent chip shortages. The China Association of Automobile Manufacturers (CAAM) expects sales to increase only 1.3 percent this year after a 9.4 percent growth in 2022.

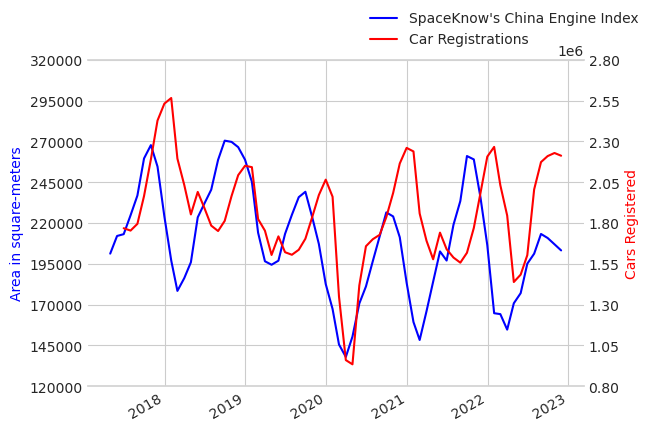

Spaceknow provides over 100 indices monitoring the Chinese automotive sector. We monitor employee parking lots, production areas where newly assembled cars are located and wait for distribution, logistic indices covering places with trucks and auto parts, and material indices that capture storage of material used during the car assembly. The Spaceknow indices can track the overall performance of the Chinese market, such as new car registrations, as visible in Figure 2, but also many individual companies, thus offering a complete picture of the market. Figure 2 shows that our index correlates well with the car registrations, and it seems to lead the benchmark by two months.

Looking at the largest Chinese state-owned auto companies – the “Big Four” – SAIC, FAW, Dongfeng, and Changan, the slowdown predicted by the CAAM is confirmed. The sales of these large brands appeared to have taken the biggest hit from the semiconductor crisis, COVID restrictions, and overall macroeconomic performance. Their growth stalled and even fell compared to the previous year. However, as these groups operate under many brands, including joint ventures with world-leading automotive manufacturers such as Volkswagen or GM, the performance can differ from brand to brand. For example, the largest Chinese automotive group – SIAC, experienced an 18 % fall in its global sales in November, while its Volkswagen brand grew slightly, and SGMW – its joint venture, capitalized on China’s NEV rise with the best-selling electric car in China.

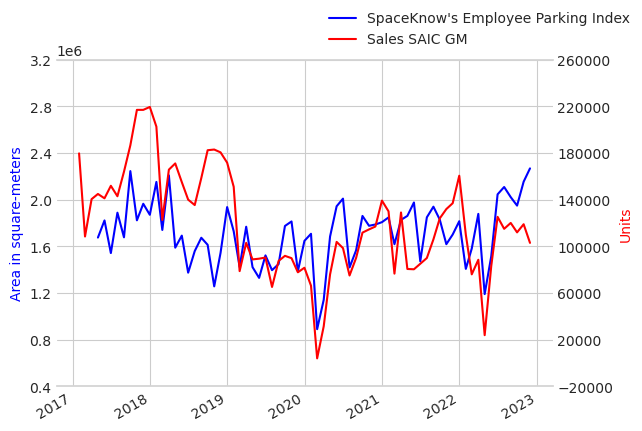

Many Spaceknow indices can match the Chinese brands’ sales/production, as shown in Figure 3 for the SAIC-GM employee parking index against the joint venture’s sales in China. We find this confirmed by looking at the statistical evidence showing that many of our indices are either cointegrated or can be used as predictors, as shown by the Granger causality test. We find similar results for FAW and Changan.

On the other hand, the market for electric vehicles (EV) is flourishing in China. While the boom period of China may be over – with its GDP growth coming back to a rate familiar to the developed economies, its EV industry is just starting to expand. This is largely caused by the Chinese government’s robust subsidy program and tax exemptions. This allowed the creation of many new smaller and purely EV-focused brands to enter the market and become highly competitive. The result is that Chinese EV brands already represent more than half of global EV sales. Global brands are facing increasing pressure from the domestic competition in China – with a rising domestic brand BYD surpassing the sales of Volkswagen in November, causing some of them to reconsider their strategy in the country. China is also ideally positioned to become the world EVs leader because of its strong position in the battery industry.

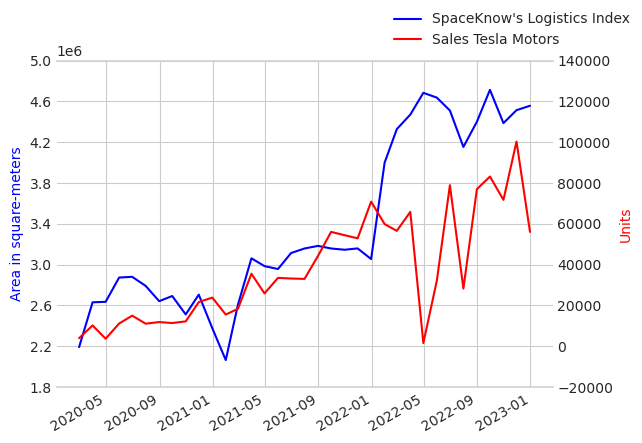

Spaceknow has indices focusing on the developing Chinese EV market. Our products include indices monitoring aspects of Tesla production on various sites worldwide. Among those indices are those from its Shanghai Gigafactory. Figure 4 shows the SpaceKnow logistics index showing the area covered by supply trucks in Tesla’s Shanghai Factory. We can see our index follows both the trend of the sales but also the large fluctuations in the company’s performance in China. The relationship seems to break with the spring Shanghai lockdown between March and May, 2022. The logistics index rose steeply during that period. Compared to Figure 1, we see that while Tesla’s workers were staying at home, the trucks used by the company for transportation of vehicles and cars were massing near the factory.

Part of the recent buzz around Chinese automotive is also a reshuffle in the government policy towards the joint-ventures. As already mentioned, joint ventures are a key part of the Chinese auto industry, and all the big state-owned conglomerates are deeply involved in multiple collaborations with US, European or Japanese counterparts. One of the examples can be found in Figure 3, where we show index monitoring SAIC JVs with GM. It was SAIC’s collaboration with Volkswagen back in the 1980s that started the whole practice of JVs. Joint ventures were crucial for getting foreign know-how into China and are now about to undergo radical changes – the strict limits on ownership share and number of JVs per foreign brand are to be stripped to increase export numbers for foreign brand cars manufactured on Chinese soil. These regulatory changes can be understood as an ambitious and successful push toward export oriented industry – China has already overtaken Germany and is about to become the second biggest car exporter (in terms of volume) in 2022.

Nowhere is the push to exports more evident than in the case of electric vehicles – heading primarily to new markets in Europe. The reason for this is also the high cost-competitiveness of Chinese models compared to European EVs and the relative openness of the European market compared to the US, which keeps high duties on Chinese cars. This leads to high pressure on European manufacturers, who are about to face a wave of affordable Chinese cars that are more competitive in terms of quality than in the past. On the other hand, the Chinese EV market is also vital for European manufacturers – VW EV sales doubled in the country in 2022. The importance of the Chinese market for European car makers can mean that the EU market will remain open in the future.

The Chinese automotive industry is an example of spectacular growth over the past decades. Despite China’s macroeconomic slowdown, the Chinese government’s commitment to energy transformation promises to transform this rapid energy into a new sector of New Energy Vehicles and a strong export push. Fomenting the NEV market may be a step towards creating a greener car sector but also a massive opportunity for new entrants, possibly allowing for a reshuffle in the car market in China and worldwide. Spaceknow follows the development of Chinese automotive and is actively expanding its light vehicle manufacturing dataset for New Energy Vehicles. We aim to focus on the key players in the Chinese energy transition, such as BYD or SGMW, and to complement our current Tesla indices and more traditional Chinese producers.

Thank you for reading, did you find value in this article? Share it with a friend or colleague.

Disclaimer

This report is provided by SpaceKnow, Inc. (“SpaceKnow”) pursuant to the following terms and conditions:

Industry data and reports published by SpaceKnow (“SpaceKnow Reports”) and made available to paid subscribers and/or other recipients (collectively “Recipients”) are creative works of the mind achieved through algorithmic analysis of publicly available data and the information therein is proprietary to SpaceKnow and protected by copyright. Any copying, distribution or reproduction without the prior permission of SpaceKnow is strictly prohibited.

SpaceKnow Reports are confidential and nothing therein may be disclosed, reproduced, transmitted, distributed, sold, licensed, or altered, in whole or in part, without SpaceKnow’s prior written consent. SpaceKnow reserves the right to release to the public at any time the data and reports provided to Recipients. No rights in SpaceKnow Reports or any of the information contained therein are transferred to Recipients. Any misappropriation or misuse of the information in SpaceKnow Reports will cause serious damage to SpaceKnow and money damages may not constitute sufficient compensation to SpaceKnow; consequently, Recipients agree that in the event of any misappropriation or misuse, SpaceKnow shall have the right to obtain injunctive relief in addition to any other legal or financial remedies to which SpaceKnow may be entitled.

SpaceKnow Reports are based only upon its algorithmic analysis of publicly available data and do not use or rely upon any material non-public information (“MNPI”). The insights included in SpaceKnow Reports do not constitute MNPI or inside information and SpaceKnow is not an insider. SpaceKnow Reports (1) may contain opinions based on third party sources that are not independently verified for accuracy or completeness, (2) may contain forward- looking statements, which are identified by words such as “expects,” “anticipates,” “believes,” or “estimates,” and similar expressions, and (3) are current as of the date of publication but may contain information or statements that are subject to change without notice. SpaceKnow has no obligation to, and will not, update any information contained in SpaceKnow Reports. Actual outcomes could differ materially from those anticipated in SpaceKnow Reports. As a result, the use of SpaceKnow Reports is at Recipients’ own risk.

SpaceKnow and its owners, affiliates and representatives are not (1) investment advisers, commodity trading advisers, broker-dealers, financial analysts, financial planners, or banks, (2) compensated for providing investment advice, (3) registered or licensed with any regulatory body in any jurisdiction as investment advisers, commodity trading advisers, financial planners, broker-dealers, or in any other capacity (including, without limitation, the U.S. Securities & Exchange Commission (the “SEC”), the U.S. Commodity Futures Trading Commission (the “CFTC”), the U.S. Financial Regulatory Authority (“FINRA”), or their equivalents in non- U.S. jurisdictions), and do not recommend the sale or purchase of securities or commodity interests, or (4) licensed or able to provide investment advice or respond to individual requests for recommendations to purchase or sell any securities or commodity interests. No regulatory body in any jurisdiction (including the SEC, CFTC, FINRA, or a regulatory body of any state or any non-U.S. jurisdiction) has endorsed SpaceKnow or the contents of SpaceKnow Reports or the accuracy, adequacy, safety, reliability, usefulness, quality or legitimacy of any information provided to subscribers in SpaceKnowReports. SpaceKnow Reports are not intended to constitute investment advice. SpaceKnow is not an investment adviser within the meaning of Section 202(a)(11) of the U.S. Investment Advisers Act of 1940, as amended, and is not a commodity trading adviser within the meaning of Section 1(a)(12) of the U.S. Commodity Exchange Act. SpaceKnow does not provide investment advisory, portfolio management or financial planning services. The analyses, forecasts, metrics, samples, estimated figures, trends, figures, tables, graphs, projections and other forms of data that may be contained in SpaceKnow Reports do not represent or contain any recommendations to buy or sell any security or any financial products and should not be relied upon as the basis for any transactions in securities.

SpaceKnow Reports are for informational, promotional, educational or evaluation purposes only. Any information contained in SpaceKnow Reports constitutes the opinion or forward-looking statement of individuals and is provided without any representation or warranty of any kind. Neither SpaceKnow nor its directors, officers, employees, agents or representatives shall have any responsibility to you or any third party for the accuracy or completeness of any information provided in any SpaceKnow Report.

Should you have any questions, please contact us at SKNowcastingSolutions@spaceknow.com.